Mastering Insurance Challenges

Running a SCR standard model under Solvency II is simple financially, but managing 1.5 million positions with granular results is complex.

Internal model Solvency II

Using our high-performance Algorithmica Risk Management System (ARMS) simulation engine, insurance clients can run large-scale simulations with 200K+ samples in minutes. Look-through adds a factor of 10 in the number of positions to simulate. The solution is in-memory simulation with our distributed calculation technology and ultra-fast result writers, delivering position and sample-level results to downstream applications. It runs on standard Windows servers and is optimized for Intel’s latest chipsets.

Large scale SCR calculations

Running SCR standard model under Solvency II is not complicated from a financial perspective. But running +1.5 Millon unique positions and aggregating across all modules and getting granular results back to the user is not trivial. Our insurance clients benefit from running SCR Solv II model using ARMS standard transaction interface which leverages of its parallel calculation capabilities. The standard model and internal model can both be run on the same set of positions, as well as ad-hoc stress tests and other risk measures needed.

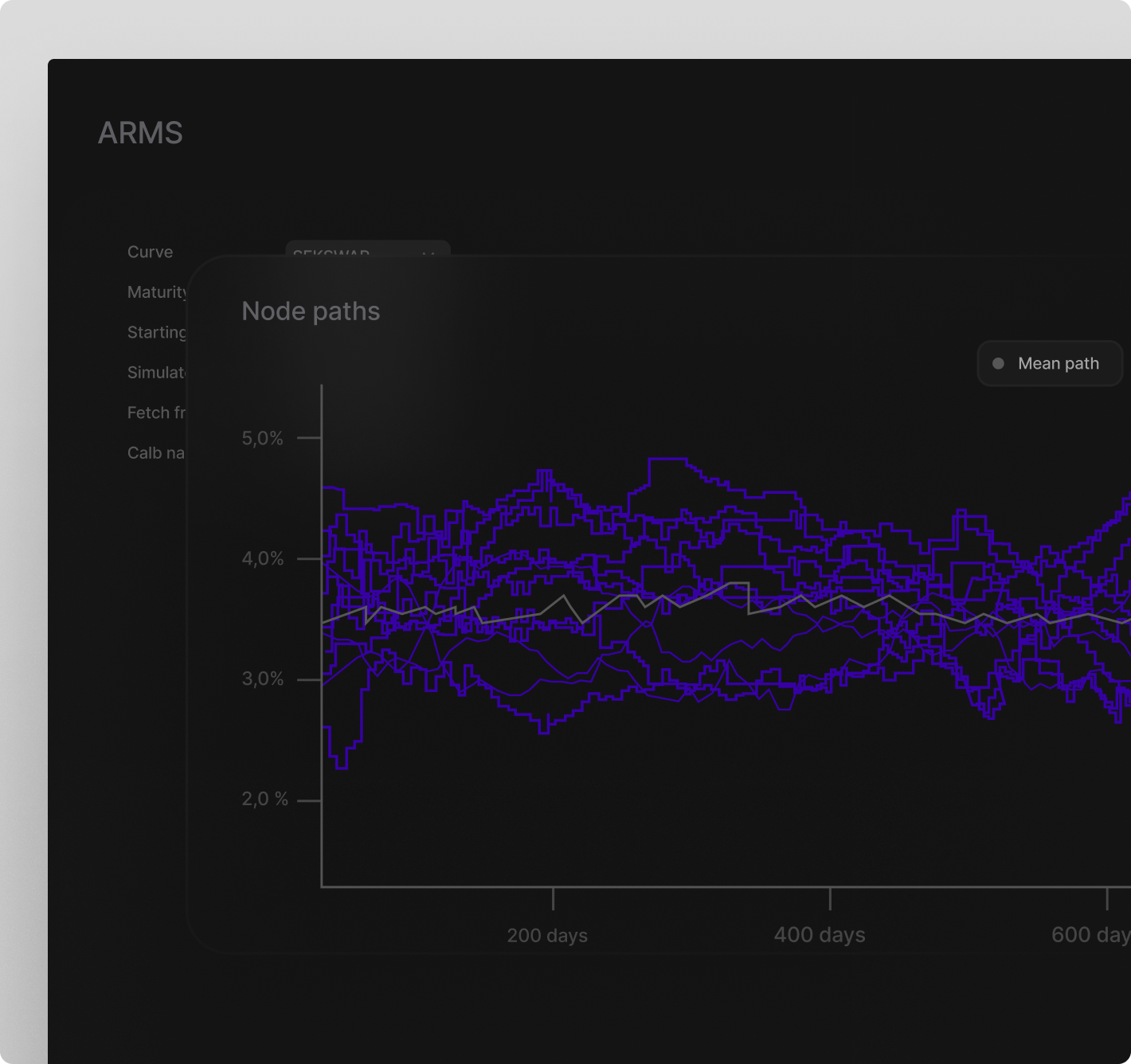

Creation of inhouse ESG samples

Using a host of models, clients needing sets of Economic Scenario Generations can create their own using our ARMS ESG module. From a dynamic set of historical market data, calculated and stored in the History Server, future scenarios can be generated using automatic historical calibration or by setting manual parameters. We support both market neutral and real world distribution.

Statistical modeling in Quantlab

Insurance clients can benefit from using our integrated coding and visualization environment to run ad-hoc calculations or creation of production quality models. Quantlab comes with a built-in statistical library, with the possibility to extend with internally created libraries written in Qlang or by simply adding third-party models using the Quantlab API. If problems involve any discounting, our fast and stable implementation of Smith-Wilson can be used together with swap market quotes from major vendors.