Quantitative

Analytics

Algorithmica provides real-time analytics and risk management solutions for better trading, improved pricing and reduced application development times.

Major financial institutions

trust Algorithmica

For three decades we have delivered software solutions for capital markets, hedge funds, exchanges and investment management firms. Our solutions are used for quantitative analysis, trading and pricing of financial instruments, risk and data management.

Our products

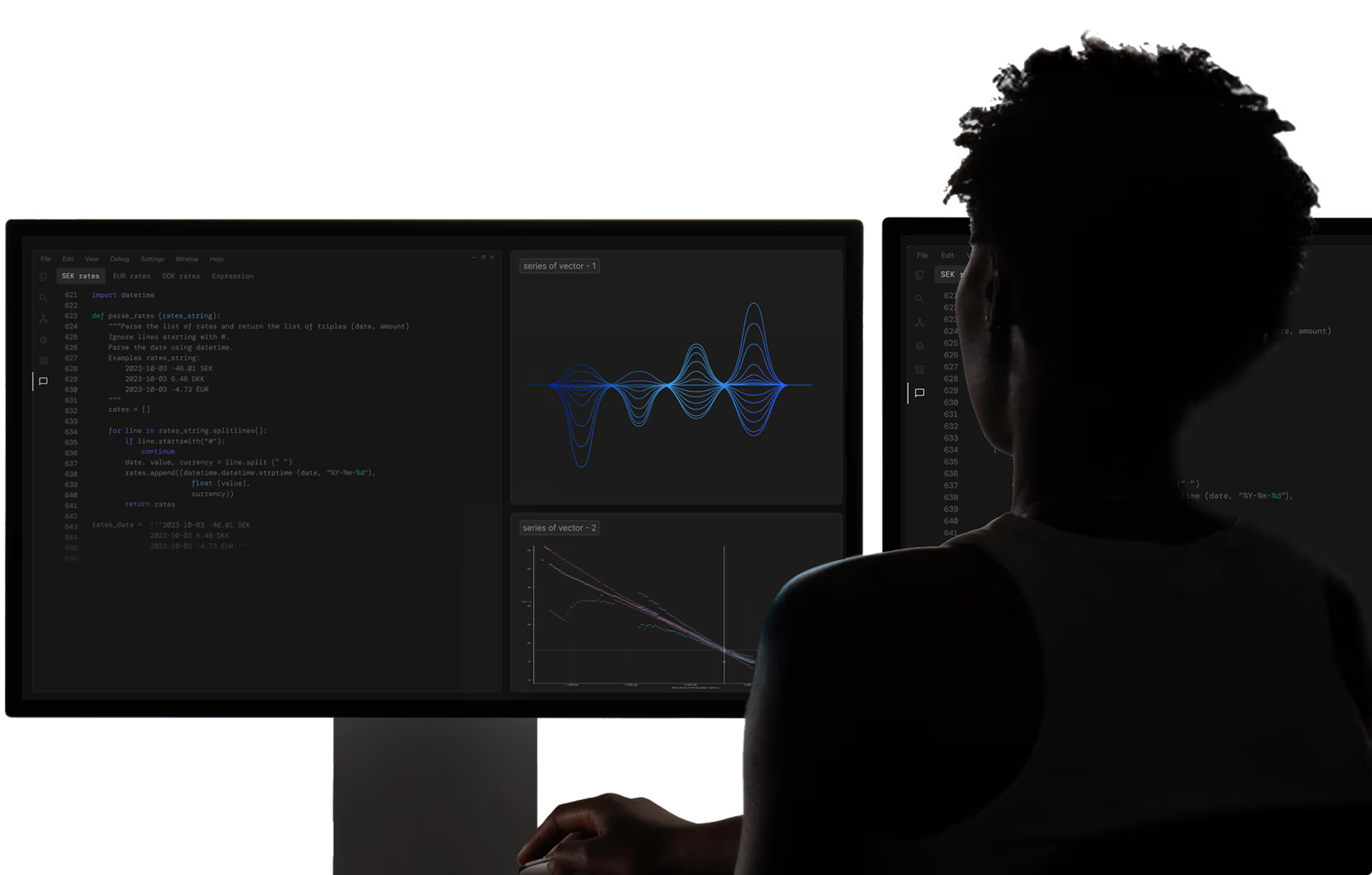

Quantlab

Powered by our lightning-fast Qlang technology and extensive library of over 8,000 functions, Quantlab is used interactively for ad-hoc analytics or to implement solutions for the trading or sales desk.

Algorithmica History Server

Algorithmica History Server (AHS) enables financial institutions to create an in-house or private cloud data warehouse from market data vendors or internally acquired data. Better data management and control means a lower total cost of ownership.

Algorithmica Risk Management System

Algorithmica Risk Management System (ARMS) performs risk analysis in real-time using in-memory technology, thereby equipping risk managers with powerful tools to

handle market and counterparty risk.

Algorithmica’s Quantlab engine is integrated into TransFICC’s TransACT service for automated pricing of swap RFQs. The solution is made available to Tier 2 and 3 banks looking for an external swap pricing engine to use with TransFICC’s GUI and workflow.

Use cases

.webp)

FAQs

Algorithmica provides high-performance solutions for real-time quantitative analytics, enabling clients to enhance pricing, trading, and risk management of financial transactions. We address our customers’ challenges through a combination of modular software products that typically work together, but can also operate independently.

Combined with our financial expertise and experience in implementing software in complex environments, this enables us to deliver cost-effective, robust, and agile solutions.

Our products include:

Quantlab: An award-winning cross-asset quantitative analytics tool for quants, traders, and analysts. Read more.

Algorithmica History Server (AHS): An enterprise-wide financial data management system offering automated quality control, cost management, and data governance. Read more.

Algorithmica Risk Management System (ARMS): High-performance market and counterparty risk management systems for traders and risk managers. Read more.

Algorithmica empowers financial professionals with tools for quantitative analysis, financial data management, and risk control. Our solutions are deployed by a range of financial institutions, including banks, asset and investment managers, hedge funds, proprietary trading firms, exchanges and trading venues.

Yes, we offer implementation, user training and ongoing support for our products. Every client implementation is different. We provide setup assistance and guidance. All our products come with comprehensive guides and manuals, and when additional help is needed, we also offer technical support and troubleshooting. Our software is continuously being enhanced.

Algorithmica is headquartered in Stockholm, Sweden, with additional offices in Denmark, Germany, Norway and United Kingdom. The best way to contact us is to send a message to sales@algorithmica.com or give us a call. You find the telephone numbers here.

In June 2024 Algorithmica was included in the QuantTech50, a respected ranking that assesses capabilities across pricing, market risk, modeling, and analytics. Besides ranking Algorithmica was honoured with the Computational Award for Time-Series Analysis Frameworks, underscoring our expertise in quantitative financial analysis and advanced computational methods. Read more.

With the installation of Algorithmica Research’s IRRBB Solution we will leverage our current market risk installation giving substantial advantages when calculating IRRBB both in speed, efficiency and flexibility.

Algorithmica has performed well in its key markets, thanks to its robust analytics and ongoing innovation.

We are very pleased with the results of our collaboration with Algorithmica. Clients are demanding more control over their data, and more transparency on the provenance of the data that they use.

.svg)